If everyone’s credit score falls, aren’t we all set?

Or is every single service in the USA that depends on credit score all going to tank at the same time?

What do you mean by soon?…mines been nonexistent for years, decades now!

Joke’s on them, my credit score already sucks. I love it when some bill collector threatens to ruin my credit. Good luck, loser.

“You have until 5pm today to take a 20% off discount on your settlement payback. If you don’t respond it may reduce your credit score.” ¯\_(ツ)_/¯

LOL @ credit scores, the US is changing slowly in a western China.

And you just keep playing along with it like good little minions.

Not the arbitrary made up numbers that some how go down every time I pay off a car loan!!!

I remember paying off my car loan years ago and it dropping. I’m like… wait a minute!

It’s crazy to me. I just focus on my personal debts and pay off timelines and ignore my credit score these days.

Banks were willing to give me mortgages a couple of months ago that I in no way could afford based off my score (it’s actually good). None of this is grounded in reality; prior to 2020 those same fucks wouldn’t even pick up the phone for me.

My credit score has consistently been around 750 for a long time and it never helped me in any way at all, anyway.

Mine’s been consistently 800+ for years… and it has helped me considerably… repeatedly.

I have one single credit card that I use and pay back regularly. I have no other debt - school loans are paid off, cars are paid off, never late on bills, rent paid on time (they report it to credit bureaus)… I don’t even have medical debt.

And yet my credit is mid 600s.

Make it make sense.

One card at $5k limit (making this number up, only you know what you’re approved for on your card) doesn’t necessarily show worthiness for holding more debt. I have 4 active cards… aggregating about $40k of revolving limits. Of course rarely ever use them and pay them down.

Holding no non-revolving debts can actually hurt you. If you haven’t had a car note or mortgage in a long time, they don’t know if you’re capable of holding such debt effectively anymore. Before we bought a house, I specifically held onto the car notes and only paid the second car off after we secured the mortgage. Of course with a mortgage, I’ll be sitting on “debt” (really building equity in the house) for a while. but meeting the terms of that debt monthly only strengthens evidence that I can manage debt correctly, increasing score.

Edit: For you, try to increase your limits on your card. If not take out another card and make a purchase every few months on it to keep it active. As you increase the “allowances” you have, and keep that in check… you’ll find your number goes up quite quickly. As far as non-revolving debt, don’t take out a loan if you don’t need it, but think about sitting on a loan for your next purchase even if you have the cash on hand to build the credit up.

I paid off my last car in 2021. I have no plans for another car payment. 10 years over 2 cars was long enough. I’m nearly 40, married with kids, neither of us have any debt, and we pay our bills on time. And yet my fucking RENTAL still required me to have a fucking COSIGNER. That’s an absolute embarrassment.

Holding no non-revolving debts can actually hurt you.

IDK about you, but I’m sick of this game. This is bullshit, the system is clearly stacked against “the poors”. There is no light at the end of the tunnel. My only source for any sort of actual savings is bonuses and bi-annual “3 paycheck” months.

I’m lucky enough to be able to put 3% of my gross pay into a 401k.

I mean fair enough on the sentiment. I’m not particularly rich. But I do well off for myself and we live comfortably within our means.

But if you don’t “play the game” don’t be mad when you don’t score well? I know it sounds harsh, but it sounds to me like you don’t actually need credit access… so why do you care then?

I think you misunderstand. I had to have someone cosign for my RENTAL. The rental I’m living in right now. DESPITE the fact that I played the game for years. DESPITE the fact that I pay all of my bills on time. DESPITE the fact that my debts were paid on time.

“Playing the game” has clearly put me in an arguably worse spot than I was when I started. I didn’t need a fucking cosigner for a fucking rental apartment when I was 20 with zero credit history.

I didn’t misunderstand. You can’t claim you’re playing the credit game and only have one credit card and no non-revolving debts for years.

And no it hasn’t put you in a worse spot. “No credit” is effectively equivalent to “shitty score”. You didn’t need a cosigner when you were 20 because that was probably decades ago when credit score wasn’t used as a metric.

Has it though? I wonder how the deals you got compared to the person who posted above you? You really wouldn’t know. Maybe you got the same deal but you are happy with it and they are not. There is no transparency.

My score never really seemed to make a difference when I financed things. I have had good and bad scores over the years. For me it’s usually based on what I am buying and how much I am willing to put down.

Generally 750 and above are considered the same, but even if they weren’t, it’s not about getting a “deal” in terms of a cheap purchase price on a car but rather cheap interest rates along with all the other crap they’ve tied to it lately like jobs and housing. With loans, you can see what the prime interest rate is for a specific type of loan and you should be getting close to that if you’re in the market for one. You’re not simply reliant on what some car salesman tells you that you qualify for (in fact this is a good way to get a terrible rate) but you can shop around yourself at banks and CUs to get the best rate for example.

Has it though?

Yes it has… because I’ve attempted to take loans primarily under my wife who doesn’t hold as high a score as I do for a myriad of reasons. Same shared incomes… same shared assets. Only difference is my score is higher as far as they’re concerned.

Jokes on them cause I don’t even have credit.

What’s all this about buying now and paying later?

Don’t do that.

I haven’t given a thought to my “credit score” in decades. I hope that means that it’s tanked due to the unimaginable, unearthly, inhuman crime of not routinely borrowing money.

Just remember, the rich are rich because they borrow other peoples money. You just need to know how to take advantage of it to work for you.

Build credit by never paying any minimum late > gain credit above 700 (ideally 750+) usually within 2-5 years > get great rates > 0% for X months starts showing up > Use their money to keep credit high, gain rewards/miles, etc.

It really just takes organizing and consistency. It’s not that hard once you’ve built the habit. In fact, my wife and I don’t even out brain power into it anymore. Credit fluctuates between high 700s / lower 800s and we get 0% financing offers constantly. Once you’re a sure bet everyone wants you to finance/get credit with them. This absolutely pays off over time. When someone else is stuck buying a car with a higher APR, I’m getting close to fed rates, same with mortgages.

Is the system perfect? No, but it’s what we all have so you may as well take advantage of its potential benefits.

When someone else is stuck buying a car with a higher APR, I’m getting close to fed rates

One of the tactics I picked up in a book on financial management was to start paying myself some kind of money as a monthly payment instead. You do that by…either lucking out and having parents that bought you a car and drive that for as long as possible, or you (like me) buy some total shitbox, either paying off the entire thing at sale or nearly immediately, and keep that on the road for as long as and cheaply as possible, all while making “payments” on my next car. Trust me, that first car especially will not be glamorous.

Then, with the money you paid yourself for whatever time - use that to buy the next car. I haven’t had a car loan in years as a consequence of this.

Paying for everything in cash isn’t always the smart financial decision. Would you rather take a 2% loan on a car and put $30k into the market earning 15% or take that $30k and earn 2% by paying for a car in cash? This isn’t true all the time especially right now, but that was the smart move just a few years ago. Think about all the people with 2.5% mortgages right now who didnt wait to buy with our current 6%+ mortgage rates.

Flipping cars from a shit box to get to high end is certainly one way to help with this. I personally never did that but know those who did.

Credit scores could end up being 20 or more points lower, according to financial experts

This, uh… doesn’t sound terribly impactful? My score fluctuates ±50 points just from regular credit utilization, idk what throwing 60k in student loans onto the report would do but - 20 points sounds very optimistic.

Not only is a 20 point drop nothing but if everyone’s score drops 20, nothing has changed.

A 50pt fluctuation is wild, like honestly you should look into why. Getting a mortgage didn’t affect my score by 50pts…

The -20 probably assumes you’re still making the loan payments.

So I checked my history and you’re right, over the last 2 years the wildest swings I’ve had have been ±20, but I also haven’t spent wildly on the cards like I used to, not exceeding 50% utilized in this timeframe.

But I think a mortage being a secured loan probably reduces impact too.

(I’m not a banker or finance person, just someone who’s watched their score rollercoaster on apps in my less responsible youth lol)

50% utilization is still enormous. Mine rarely goes above a few % pts

Some credit card companies will change your credit limit after you make a large purchase, so that no matter now much you pay off, you’re always just under your limit.

Are you checking your credit score through your bank? My bank offers that kind of thing but it’s not all that accurate. I see mine go up and down Randomly. I paid off loan early and it dropped about

1026 points. It went back up, and is usually always hovering around the same spot.Edit: actually went down 26 points during the month I paid off some Loans,holy shit

It makes sense that your score went down when paying off loans. I have heard that closing accounts, credit lines, and phone plans do the same too. Supposedly because now theres “less history” of your good credit, or maybe just because of lower credit utilization.

That’s so ridiculous. Either way, it’s back up again but that drop was kind of a shock.

Credit scores aren’t just about how likely you are to pay back loans, they are about how much money can be made off lending to you.

Pay off loans early, and the lender makes less money, so your credit goes down.

Closed accounts, inactive accounts, those aren’t making anyone else money, so less credit score.

Paying on time is the biggest risk of lending, so it has the biggest impact, but doing things that lose your creditor money can make a difference on the margin.

Credit reporting is an evil practise. It needs to end.

Before credit reporting credit decisions were literally determined based on vibes, which of course means rampant discrimination. While I can think of additional protections and reforms to credit reporting, I’m not sure there is a better option for determining credit risk than a centralized credit reporting mechanism like we have now

I don’t have a specific policy proposal for you. Needing a long term loan to have access to transportation or a place to live is already a pretty grim situation, but building a punitive and dystopic privacy nightmare on top of that doesn’t really meet my criteria for “unpleasant but necessary facts of life, might as well accept it”.

We’re miles away from a sane reality, and all I’m doing is pointing that out - we’re not going to have a good time whether we decide to accept it and let things get worse or start fighting our way back. It’s all a nightmare.

Credit reporting is an evil practise. It needs to end.

What should lender use instead to determine you are capable of paying back money you’re asking to borrow from them?

How about we don’t build an economy on borrowing?

I’m not an economist, but I’m not aware of any economic systems that work without a lending component.

Without lending that means you’ve got one group of people with stuff that don’t need it, and another group of people with need for stuff but without stuff. Without lending there’s no way for the people with needs to get stuff, and the stuff is wasted sitting without being used.

Thats the world you want to live in?

Money is credit. It’s a promise that someone else will pay their labor or capital or goods in exchange.

I would like a world where the things people NEED housing, food, medical care, are provided and the things people want, they can save up money (credit) and purchase by selling what they can, labor, skills, assets.Well usury is harem in Islam, so you can do it without the insane profiteering.

So your problem isn’t lending, its just large profits on lending?

Yeah pretty much. It’s just, in a capitalist system (without some kind of overarching ideology shaming people into not doing it), there is no lending without profiting. Nobody is going to lend their money out of the goodness of their heart in this system.

Though mutual aid could probably solve this.

There in lies the confusion.

A credit score doesn’t tell a lender if you will pay back a loan. A credit score tells a lender how much off a guarantee it is to make money of lending you money.

A credit score doesn’t tell a lender if you will pay back a loan.

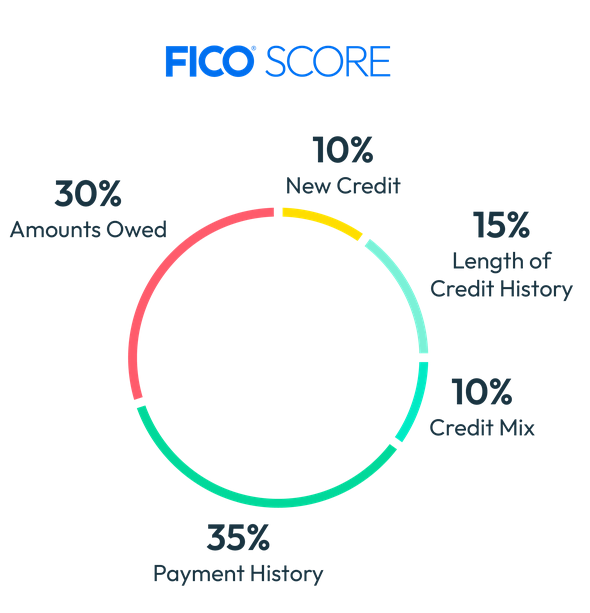

Well, nothing is a guarantee in life. However, that’s exactly what its designed to do. It provides the recent history of the borrower and how much debt they are carrying now to show that the borrower is capable of servicing the debt. All of the included factors go into the score. I mean, the components of the score are not a secret. Is publlished right on their website:

A credit score tells a lender how much off a guarantee it is to make money of lending you money.

Kind of. If the borrower is bad at paying back debts, then the lender increases the interest rate to cover the likelihood the borrow will default on the loan. Keep in mind, they aren’t trying to get all of their principal back from the risky borrowing through interest before the borrower defaults. This risky borrower is pooled with other risky borrowers. The higher interest rates they all pay covers the few that default.

Accept the risk and pay the cost of the defaults. If lenders would have it their way, they’d only lend to people who pay back and charge them interest on it for the privilege, which would be pure economic rent.

Accept the risk and pay the cost of the defaults.

Do you honestly think any lender would stay in business very long if they did this? Especially if there were no consequences to borrowers, (such as a what exists today with a credit score hit that would prevent you from borrowing in the future) why would anyone pay back a debt?

There are problems with credit reports and credit scores, I agree. Medical debt and perhaps even student loan debt shouldn’t be on there. However, throwing out the whole thing makes life for most everyone significantly worse, except the rich. The rich will do fine because they have substantial assets to use for loan collateral without any credit scores. How about you? What property would you be able to put up if you needed new car or wanted to borrow for a mortgage?

If lenders would have it their way, they’d only lend to people who pay back and charge them interest on it for the privilege, which would be pure economic rent.

You’re describing borrowing before credit scores. Or at best any unsecured lending was for only very small balances, such as few hundred dollars. So no credit cards with four or five figure credit limits. Mortgage lending with a required a 20% down payment. No 20% cash? Enjoy renting. Before the Great Depression it was a required 50% down payment, and you only had 5 to 10 years to pay off the other 50% or they came and took your house and kicked you out in the street.

Oh, and we think interest rates are bad now. My parents were paying a 12% mortgage interest rate in the 1980s. Do the math on that today to see how much that would increase a monthly mortgage payment putting home ownership even farther out-of-reach of many.

This is the future you’re wishing into existence, a return to the “bad old days”. If you get your wish, getting ahead for the average American gets harder, not easier.

It would crash housing prices, which would be objectively good. I can’t say for certain if it would be worth the other costs.

But with no ability to borrow to buy those, then cheap, houses, who would buy them and why? Sadly the answer would be: those with cash so they could rent them out.

Collateral and, historically, age, race, sex, and ethnicity. They’d also look at how well you were dressed because 100% of the time you went to the bank in-person to get a loan. Also, your bank wouldn’t be far from where you lived and the local population wasn’t so large that they couldn’t just “ask around” the local social network to see if this man before them was upstanding enough to warrant giving them money.

Also note that people didn’t need to borrow money as much as they do today. You wanted a new home appliance like an oven or refrigerator? You saved for quite some time to buy it.

There weren’t as many things to spend your money on either!

I’m a bit confused by your response. Are you suggesting going back to the old ways (as your description of those old ways encapsulates) or are you pointing out the shortcomings of the old ways (of which there are many)?

I’m just telling it like it is. The old ways were terrible! However, being local and requiring proper collateral instead of just giving n people money en mass—knowing that the percentage that default will be outweighed by the percentage that pay the loan back (and ripping people off by making them pay the interest up front)—was probably better for the economy.

Not everyone should be allowed to amass debt the way we currently allow it. Furthermore, if people couldn’t get loans for school so easily (in fact, guaranteed!) then college tuition would be but a fraction of what it is today.

It’s there for good reason. Credit can be used for good or ill. Just remember, anything can and will be gamified. We humans love patterns and puzzles too much.

Who would be likely set something like this up without the desire to use it for social control? The government? China’s system. Capitalists? Ours. It exists to incentivize you being in perpetual debt that can be leveraged over you by those who own everything. It’s a system that ensures indentured servitude; a system for the wealthy to project power over you. What fucking entity would have selfish motivation to do anything more?

Credit scores are barely a 40 year old concept

There is far more corporate and institutional fraud rather than individuals causing problems

“There are 45 million people with student loan debt and 15 million with medical debt. It’s highly likely that there is some overlap there,” said Adam Rust, director of financial services for the Consumer Federation of America. “People are really facing a perfect storm here.”